Minimum Wage Increases will Drive Change

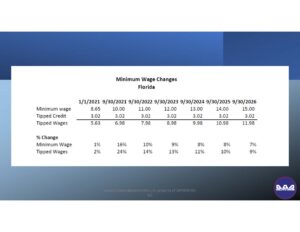

Over 30 states have enacted minimum wage laws that push the state minimum wage above the Federal wage ($7.25). Many of these states are on a schedule to increase the minimum wage to $15/hour, including Florida. Florida will reach the magical number in September 2026.

Businesses will adjust to these cost increases. Including:

- Increasing prices to the consumer

- Deploying automation

- Reducing employee count

- Change to Service Charge model, and away from the tipped employee model

The current tip credit allows employers to pay tipped employees a reduced minimum wage. Businesses may consider eliminating the tipped wage in favor of paying regular minimum wage and using a service charge method. as a way to adjust to the increase in wages. Making this choice warrants careful consideration given the financial benefit it provides the employee and the employer.

#1 – Before making the choice to not use the tip credit and FICA Tip Credit, consider the total financial impact. These offer the employee and employer a HUGE financial benefit.

#2 – The current proposed Federal legislation for $15 per hour minimum wage does NOT provide for a tip credit nor FICA Tip Credit. This will eliminate your choice and impose HUGE wage increase and loss of tax credit.

A tip credit is a legal reduction in minimum wage rate paid to tipped employees and allowed by many states, including Florida. Notice that for Florida (schedule above) the tip credit remains the same at $3.02 even though the minimum wage increases. Florida will see a

116% wage increase for tipped employees if the Federal minimum wage legislation passes, a threat to the life of the restaurant industry.

Who is Eligible for Tipped Wages?

Employees that receive more than $30 per month in tips are eligible to be compensated as a tipped employee. This applies predominately in the restaurant industry, and even more specifically to the Full Service Restaurants (FSR). Cooks and back of the house employees normally are not paid as tipped employees since they don’t meet the requirement. And, Quick Service Restaurants (QSR) have few if any employees classified as tipped employees.

How are Tips Reported?

Tips are treated as if they are received by and owned by the employee. So, the employer does not report tips as revenue and does not pay income tax on the tips received by the employee. However, payroll taxes are paid by both the employee and the employer on the total tipped wage and the total tips received and reported by the employee. Even if the employer collects the tip from the customer through the payment process and the employer pays the employee the tips through the normal pay check process, the tips received are not an ‘expense’ to the employer.

The tipped wage ($5.63 currently in Florida) is reported as an expense on the books of the employer and a deductible expense for tax purposes. Likewise, this tipped wage and total reported tips are reported on the employees’ W-2.

What is the FICA Tip Credit?

The FICA Tip Credit is a tax credit available for the employer. The credit is an offset to the employer’s tax liability reported on the employers’ tax return. The amount of the credit is based on the total tips received by each employee and the FICA tax paid on tips received that are in excess of the minimum wage. Higher tips, mean higher FICA tip credit. FSRs with higher menu prices naturally would be expected to garner higher tips for the employees which will result in higher FICA Tip Credit for the employers.

Is a Credit the Same as a Deduction?

No, a tax deduction and a tax credit are not the same. A deduction reduces taxable income. Tax liability is based on a tax % and net profit or taxable income of a business (or taxpayer). The tax liability is the amount owed to the IRS (or State).

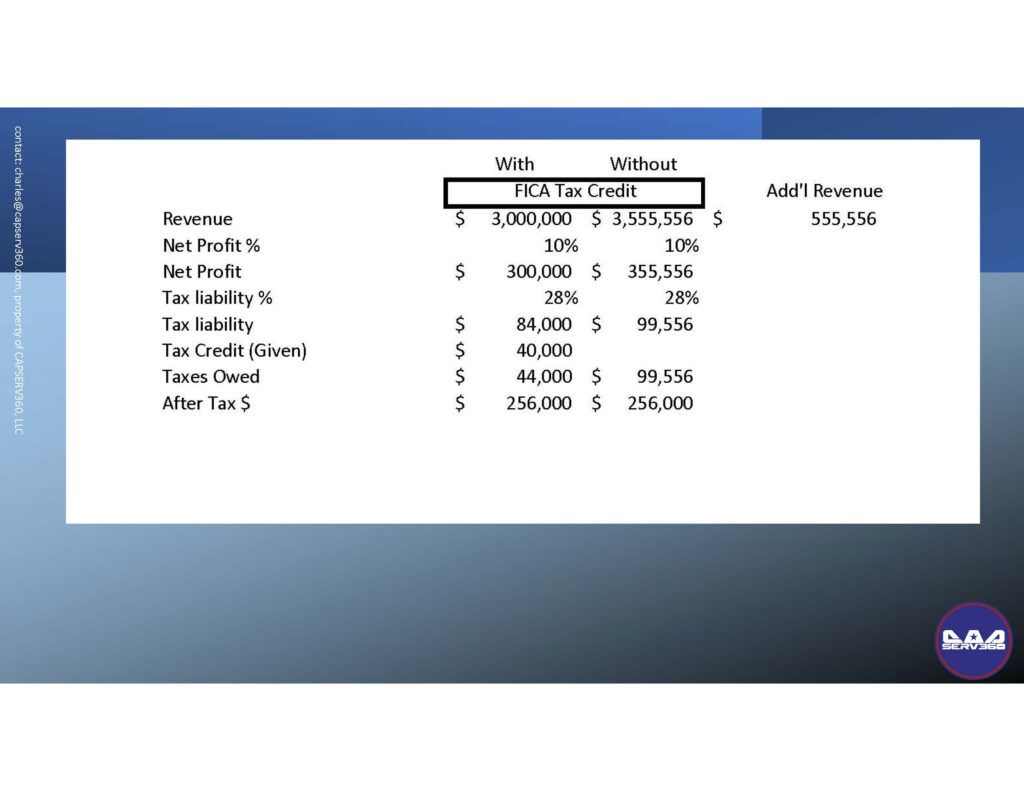

The tax credit is a dollar for dollar offset to the tax liability. The dollars left for the owner after applying profit %, income tax rates and tax credits is

after tax dollars. A goal of any business owner is to maximize after tax dollars. As an example, the chart below shows after tax dollars with and without a FICA Tip Credit. To achieve the same after tax dollars without the FICA Tip Credit, revenue would have to increase by over $555,000. This is a

19% increase in revenue greater than revenue that has the FICA Tax Credit. Seems like a big deal!

Benefits of Tipped Wages Model vs Service Charge Model

On the surface, a tipped model provides many benefits to both the employee and the employer. The FICA Tip Credit is an obvious benefit to the employer. Higher potential pay based on service level provided is an upside benefit for the employee in the tipped model. The Service Charge model removes (assuming no hybrid model) the benefits of the tipped incentive, tipped higher compensation to the employee and the FICA Tipped Credit to the employer. The employee will receive a higher wage (not necessarily a total of wage plus reported tips) and the employer now reports the Service Charge as taxable income. True, they will now have a full deduction of the compensation paid to the employee (since no tips). But, will the net increase in revenue be enough to offset the additional cost paid to the employee and the loss of the FICA Tip Credit? To have a net benefit for the Service Charge Model, it’s a steep mountain to climb. Financial models with assumptions will need to be prepared and planned. Then, trial and error of the models will most likely be necessary.

Plan and Prepare Now

The FICA Tip Credit is one of many aspects to consider when adapting to and planning for the minimum wage changes. Seek the advice of professionals when strategizing your plan. And, of course consulting with early implementers will provide a wealth of knowledge.

For assistance with your planning strategy or questions about this subject, please contact Charles Musgrove at

[email protected]

Recent Comments